Agents Pay Attention to the Settlement Statement

I have a settlement on Monday!! Yeah!! But before I did my happy dance and my rendition of the popular "another one's done, another one's gone, another one bites the dust" I give the settlement statement a once over.

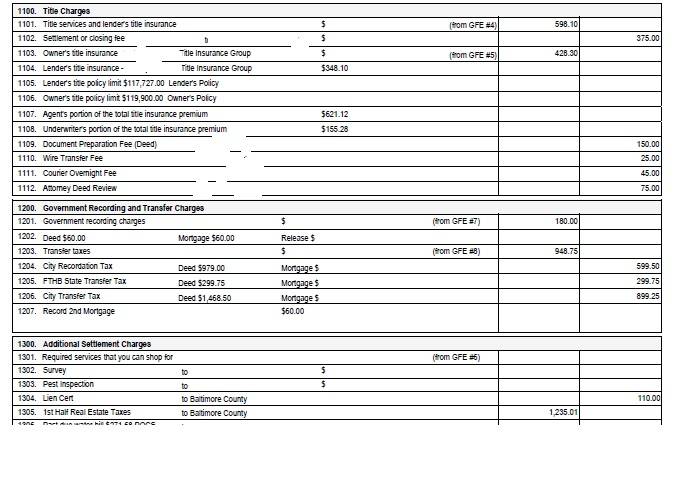

This settlement statement doesn't look right. I've been in the business a long time and I've sold hundreds if not close to a thousand homes so I've seen my fair share of settlement statements. But, I am having trouble with this one.

This settlement statement doesn't look right. I've been in the business a long time and I've sold hundreds if not close to a thousand homes so I've seen my fair share of settlement statements. But, I am having trouble with this one.

One of the best reasons for having a great relationship with your closer is that if you have a problem and even if they aren't closing your deal they will help you out. I call The Title Lady and ask her if she can quick give a look see at this settlement statement for me. In less than 5 minutes she's on the phone with me, and a few words I won't repeat here were said and the long and short of it was they had moved almost a $1000 in fees from the buyers side to the sellers side of the settlement statement and tried to tell me that's the way it's supposed to be done plus they double billed the lien certificate and over padded the water bill escrow.

First thing to look at is to make sure the sales price is right, then check your commission and any flat fees are there and that the earnest money deposit is taken from the right agent, if you aren't holding the earnest money deposit make sure they don't deduct it from your commission check (this happens a lot). Next thing is scan down your seller's side and make sure the deductions make sense.

First thing to look at is to make sure the sales price is right, then check your commission and any flat fees are there and that the earnest money deposit is taken from the right agent, if you aren't holding the earnest money deposit make sure they don't deduct it from your commission check (this happens a lot). Next thing is scan down your seller's side and make sure the deductions make sense.

On this settlement statement the property tax section is blank and I'm like "where are the property tax prorations?", they are on page 2, they should be on page 1. Then they double charged for the lien certificate, actual cost is $55 and I always see that on the buyer's side, not the seller's side. The document preparation also on the buyer's side, unless the title company has to prepare a power of attorney or do separate settlements. My seller will be at settlement so there shouldn't be a wire transfer fee, the recording fee is also charged to the buyer, the attorney deed review also gets charged to the buyer and there was no mortgage on the property so they aren't overnighting anything anywhere so that fee too should be removed.

Thanks to The Title Lady's keen eye and assistance we were able to save my seller $970.

It turns out this title company had sent coupons to some agents offering free title services except for the title insurance, to generate more business and to recoup the funds they were putting all the fees on the seller's side of the settlement statement. They confessed to having done about 1000 settlements (The Title Lady has done 47,000 settlements) and always doing it this way. Then they call me and tell me that they won't be disbursing at the settlement and now we aren't settling until the afternoon so they can pay everyone. In Maryland "dry settlements" are illegal, unless the title company can disburse at the table settlement must be delayed.

Agents, keep your eyes open and don't be afraid to ask someone to look it over if it doesn't look right and don't participate in a dry settlement, it's illegal.

Comments(3)