It’s happening and you don’t even know it. The silent increase in home mortgage rates is impacting your new custom home. If you are purchasing a home and you need a mortgage to do it, every interest rate increase means you qualify for a lower loan amount. This means you will make the exact same payment, but that payment will buy a smaller home or one with less amenities. Every time the rate goes up just a .25% means you could have lost the ability to get the mudroom you have always wanted or the granite countertop you have dreamed about. In the last six months, the average 30 year mortgage rate has already gone up .50%.

HOW DOES A LENDER CALCULATE YOUR MAXIMUM LOAN AMOUNT?

Many home buyers have the lending process backward. They approach a custom home builder and request an estimate or quote to take to the bank. They want to see if they will qualify for the house they have selected. That is actually backward. The first step for a home buyer is to actually go to the mortgage lender first! A lender just doesn’t arbitrarily pick an amount and approve you for it, there are many criteria that go into determining the maximum amount you will qualify for and the interest rate you will be charged.

A lender makes money by loaning money. Lending money to someone that won’t pay it back defeats that purpose. Lenders have a process to determine how much of a loan payment you can reasonably make each month based on your income and your other debts and then be expected to regularly make that payment on time. This formula is known as your debt-to-income ratio.

Underwriters look at your “front-end” ratio and your “back-end” ratio. The front-end ratio is your new mortgage payment (principal, interest, property taxes, and insurance, plus other items like homeowner dues if applicable) divided by your gross monthly income. So if your monthly income is $8,000 and your total house payment is $2,000, your front end ratio is 25%.

RELATED: THE SEVEN STEPS OF MODULAR HOME CONSTRUCTION FINANCING

Add your other monthly expenses, car payments that total $600 and $200 in credit card payments, to your housing costs for a total of $2,800 a month, and you have a back end ratio of 35%. This falls within most lenders’ guidelines, assuming that you have good credit and some money in the bank.

HOW INCREASING INTEREST RATES DECREASES THE HOUSE YOU CAN AFFORD

If your lender says that based on your income and debts (debt-to-income ratio) you will qualify for a monthly payment of $1,200. That is the maximum they will allow you to pay for your housing costs. But there are several other factors that determine how much money you can spend to buy your new home. They include the interest rate you will be charged, the term (or duration) of the loan, how much down payment money you have, along with some others items.

So, let’s say that you qualify for a Principal & Interest (P&I) monthly payment of $1,200 (using only P & I to illustrate – taxes, homeowner’s insurance, and mortgage insurance are not included).

Sales Price of $335,000

$1,200 per month

30-year fixed rate

20 percent down payment

Loan amount of $268,000

3.5% interest rate

So, what happens with a .5% increase in the interest rate?

Same scenario — but the rate is now 4%. The maximum sales price decreases to $315,000. With 20% down payment, the loan amount is now $252,000 or about a 5% decrease in home buyer purchasing power.

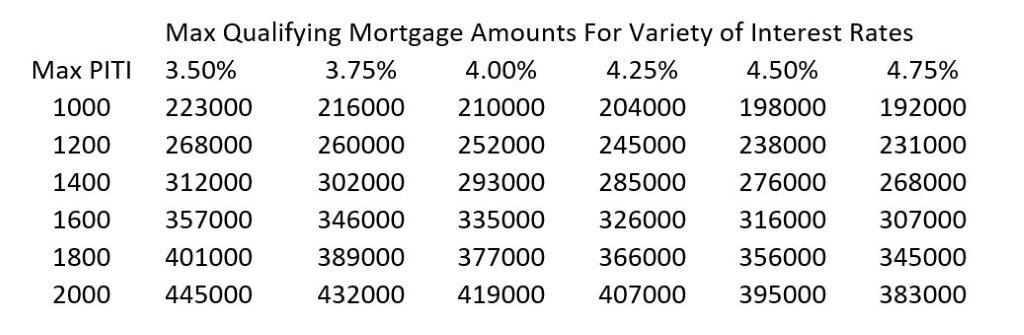

This chart shows you how a .25% or one-quarter percent interest rate increase affects a home buyer’s purchasing power. (NOTE: Monthly payments have been rounded up or down by a few dollars. APR’s are not disclosed. Chart for illustration purposes only.)

Here’s the bottom line – For every .5% (one-half) percent increase in interest rate your purchasing power may be decreased by 4 to 5 percent (the percentage is smaller for lower loan amounts). For every 1 percent interest rate increase, your purchasing power may be decreased by 9 to 11 percent (the percentage is smaller for lower loan amounts).

No one knows when interest rates will rise or how much they may increase. While we have seen a .5% increase in the last six months, who knows where they will end. Even if they rise to 5%, that is still a historically good rate. However, given current rates, that would mean your actual home purchasing power would decrease by 10-15%. That significantly impacts the home the lender will say you can afford!

THE VALUE OF MODULAR

Interest rates have gone up. The amount of home you can purchase has gone down in recent months. The one thing that remained constant is the value that modular constructionprovides when building your custom home. The construction labor shortage is continuing to put pressure on home prices. As home prices rise along with interest rates, the custom home you can afford to build is decreasing. Modular construction is the modern way to get the home you want at the absolute best value!

Comments(0)