My law practice entails a significant number of clients that come from other "short sale experts" - both attorneys, title companies and experts come lately. Sometimes (ok, many times) the client has arrived because of a troubling experience. Here is an example caused by misrepresentation that does not sit well with the client.

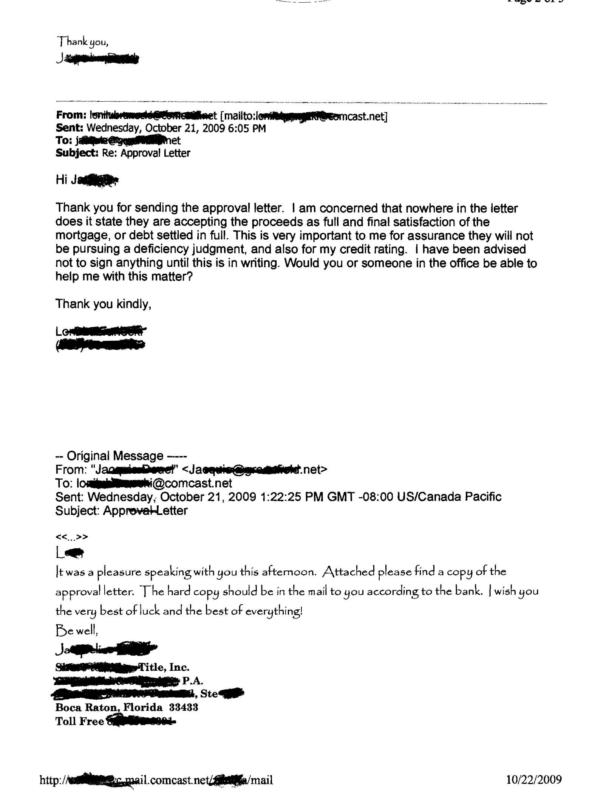

Below is a an approval letter from Third Federal that states that the lender will accept about $41,000 in the short sale provided certain conditions occur. The letter closes with no more than, "...Third Federal will release the mortgage on the above referenced property."

The often asked question of the short selling borrower is, "Is this a release of my liability under the promissory note?"

The answer is not easy to provide and many factors need to be examined.

First, does the letter state that the remaining liability for payment of any deficiency or of the promissory note, is being released or forgiven? In this letter the answer must be, no.

Second, does the letter specifically state that the mortgage is being "satisfied"? Satisfaction of a mortgage usually (but does not necessarily) includes language that the underlying obligation (the promissory note) is paid in full. Better language in the letter would be the mortgage is being "fully satisfied" or even the "mortgage and note are being satisfied". None of that language is present in this letter.

The borrower client in this letter decided to do dig around the Internet to find out what liability could exist based on the language in the letter. The short sale had been negotiated by a title company associated with a law firm in Boca Raton, Florida, and the borrower told me that the law firm was being paid at the closing - so the fee was contingent on the deal closing.

The email exchange moves from excitement of getting the approval lletter to questions about it. Out of the box on October 21 the borrower inquires about the debt (promissory note) being settled in full, and that a full settlement is of prime importance to this borrower.

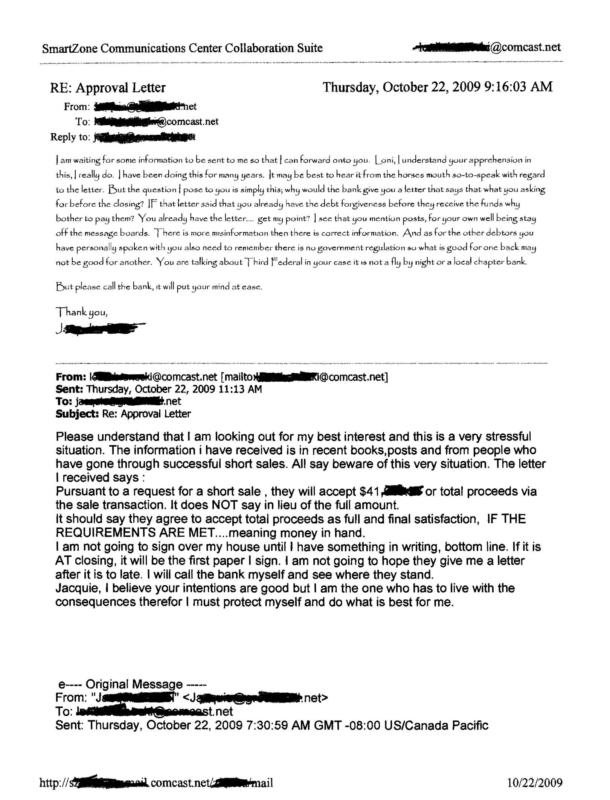

The initial response is not an answer but throws out another question - "... why would the bank give you a letter that says that what you are asking for (the release - Ed) before the closing? If that letter said that you already have the debt forgiveness before they receive the funds why bother to pay them"? This response is clearly twisted, but I cannot imagine a knowledgeable short sale "expert" dispensing this type of response. Thankfully the writer suggests the borrower call the bank. The additional emails state that AFTER the closing the bank will issue a letter to the borrower that the debt is forgiven. The short sale "expert" says you do get the forgiveness letter, but just not before the closing. Has any reader of this blog found that to be the case? I haven't as of yet.

The final response email attaches the 2007 Mortgage Debt Forgiveness Act. The MDFA does apply to forgiven debt, but the use of this information and "the beauty of all this" is totally misleading and skirts the question about whether or not the debt is being forgiven by the letter that does not contain that specific statement.

I do want to point out that some bank letters say that the lender may pursue the deficiency and those banks will simply not issue any clarification or back-off of their "may pursue" statement. However, I have noticed that usually the recorded mortgage satisfaction or mortgage release specifically states that the lender is "satisfying the lien of the mortgage having received payment in full of the indebtedness".

My clients thus far have successfully used a copy of the lender's own recorded document (the Satisfaction of Mortgage or the Release of Mortgage) to end calls from the lender's collection department for those calls that may begin after the closing. These documents seldom make it to the Broker who handled the sale as it is typically a title underwriter reviewed document several weeks after the closing.

What has been your experience? Remember, unless the deficiency has been forgiven, waived or satisfied in writing, the lender retains the right to collect the unpaid promissory note until the statute of limitations has run. See FORECLOSURE DEFICIENCY JUDGMENT or SHORT SALE PROMISSORY NOTE or BANKRUPTCY - REVISITED

Copyright 2009 Richard P. Zaretsky, Esq.

Be sure to contact your own attorney for your state laws, and always consult your own attorney on any legal decision you need to make. This article is for information purposes and is not specific advice to any one reader.

Richard Zaretsky, Esq., RICHARD P. ZARETSKY P.A. ATTORNEYS AT LAW, 1655 PALM BEACH LAKES BLVD, SUITE 900, WEST PALM BEACH, FLORIDA 33401, PHONE 561 689 6660 RPZ99@Florida-Counsel.com - FLORIDA BAR BOARD CERTIFIED IN REAL ESTATE LAW - We assist Brokers and Sellers with Short Sales and Modifications and Consult with Brokers and Sellers Nationwide! Shortsales@Florida-Counsel.com New Website www.Florida-Counsel.com.

See our easy to understand articles at:

TABLE OF CONTENTS - SHORT SALE AND LOAN MODIFICATION ARTICLES

Comments(31)